Land or Flats After GST? Choosing the Right Real Estate Asset

Since the introduction of Goods and Services Tax (GST), many homebuyers have struggled with a basic but important question: is it better to buy land or flats after GST? The tax structure has clearly changed how residential real estate is priced, especially for under-construction properties. But GST alone should not drive the decision.

To make the right choice, buyers must understand how GST impacts flats versus land, how liquidity and holding periods differ, and what risk profile each asset truly carries. This article breaks it down in simple terms, without assumptions.

GST Impact on Flats vs Land

GST applies very differently to land and flats.

For land transactions, GST is not applicable. Sale of land is treated as neither supply of goods nor services under GST law. Buyers pay stamp duty and registration charges, but there is no GST component on the transaction value (Central Board of Indirect Taxes and Customs – GST on Land).

For flats, GST depends on the construction status. Ready-to-move-in flats with completion or occupancy certificates are exempt from GST. However, under-construction flats attract GST.

As of current regulations, under-construction residential flats attract 5% GST without input tax credit for non-affordable housing and 1% GST for affordable housing (GST Council Notifications). This GST is calculated on the agreement value and directly increases the purchase cost.

This difference often makes land look more attractive upfront. However, GST should be viewed as a cost factor, not a value determinant.

How GST Changes Buyer Behaviour

GST has pushed many buyers towards ready-to-move-in flats or plotted developments to avoid additional tax outflow. This shift has improved transparency but has also widened the price gap between under-construction and completed projects.

Developers often adjust base prices to absorb or offset GST impact. As a result, the effective price difference is not always as large as it appears.

More importantly, GST does not affect long-term appreciation directly. It impacts entry cost, not asset behaviour over time.

Liquidity Differences Between Land and Flats

Liquidity refers to how easily an asset can be sold without significant price compromise.

Flats generally offer higher liquidity in urban markets. They cater to end-users looking for immediate housing, rental income, or easy financing. Banks are more comfortable lending against apartments, which improves buyer pool depth during resale.

Land transactions are more selective. While well-located plots can deliver strong appreciation, finding the right buyer takes time. Ticket sizes are higher, legal due diligence is stricter, and financing options are limited.

According to CBRE India, residential apartments account for the majority of urban housing transactions, reflecting stronger liquidity compared to land (CBRE India Residential Market Outlook).

Liquidity becomes especially important during market slowdowns.

Holding Period and Cash Flow Considerations

Land is typically a long-term holding asset. It does not generate regular income unless developed or leased for specific uses. Returns are realised mainly through capital appreciation.

Flats offer flexibility. They can generate rental income, support leverage through home loans, and be exited in phases if needed.

For buyers relying on EMIs, rental yield acts as partial support. Land does not offer this cushion.

Holding period expectations should align with personal cash flow stability, not just return projections.

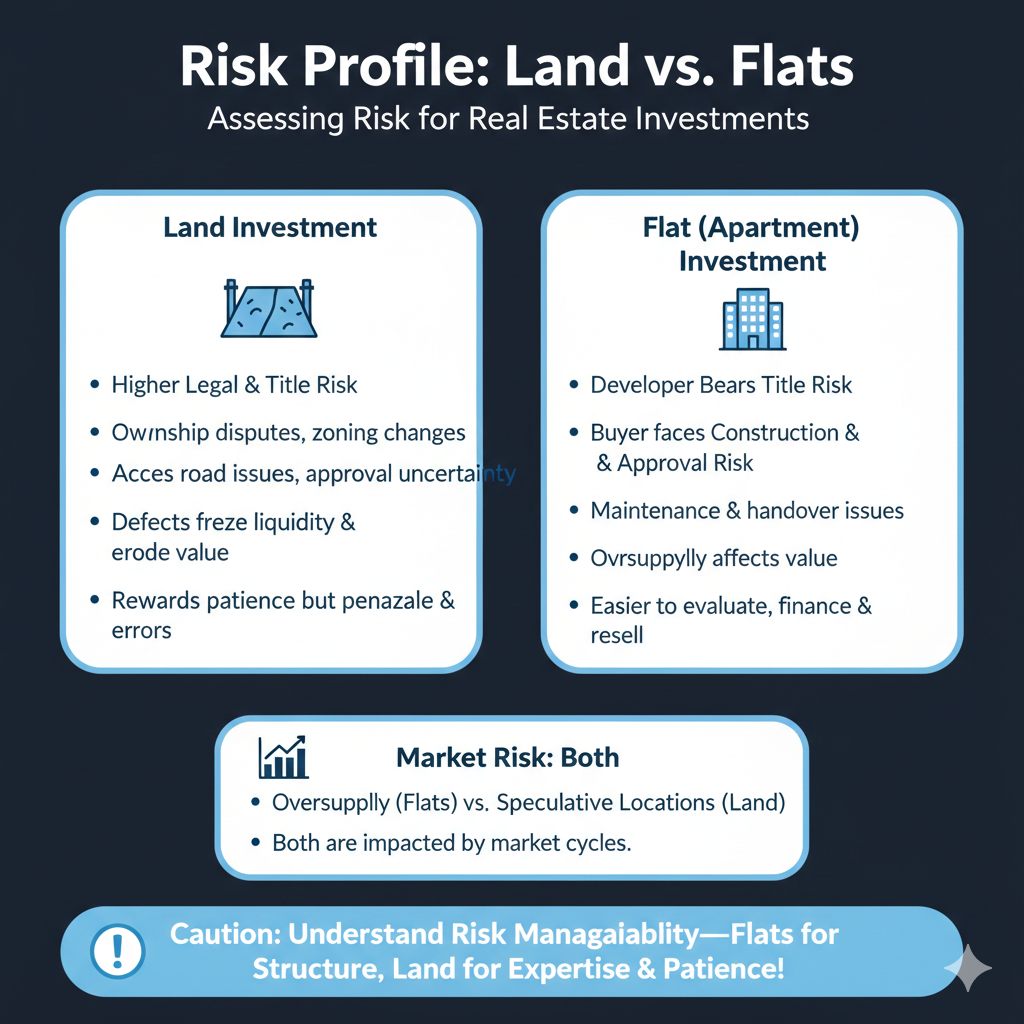

Risk Profile: Land vs Flats

Land carries higher legal and title risk. Issues related to ownership clarity, access roads, zoning, and future development approvals are common. Any defect can freeze liquidity and erode value.

Flats shift some of this risk to the developer. However, buyers face construction, approval, and maintenance risks, especially in under-construction projects.

Market risk exists in both. Oversupply affects flats, while speculative location bets affect land.

The key difference lies in manageability. Flats are easier to evaluate, finance, and resell in structured urban markets. Land rewards patience and expertise but penalises errors severely.

Which Asset Suits Which Buyer

Land suits investors with surplus capital, long holding capacity, and strong legal due diligence capability. It works best when purchased in growth corridors with confirmed infrastructure and end-user demand.

Flats suit end-users, first-time buyers, and investors seeking balanced risk. Ready or near-completion flats reduce execution risk and offer predictable usability.

GST should not be the deciding factor. Suitability, liquidity needs, and risk tolerance matter far more.

FAQ Section

Is GST applicable on land purchases?

No. GST is not applicable on the sale of land. Buyers only pay stamp duty and registration charges.

Do all flats attract GST?

No. Only under-construction flats attract GST. Ready-to-move-in flats with occupancy certificates are GST exempt.

Is land always a better investment after GST?

Not necessarily. While land avoids GST, it carries higher legal risk and lower liquidity compared to flats.

Which is safer for first-time buyers, land or flats?

Flats are generally safer for first-time buyers due to easier financing, clearer documentation, and better resale liquidity.

Conclusion

After GST, the choice between land and flats has become more visible but not simpler. Land avoids GST and offers pure appreciation potential, but demands patience and legal expertise. Flats, especially ready-to-move-in units, provide usability, liquidity, and financing comfort, even with GST considerations.

The right asset is not the one with lower tax, but the one aligned with your risk profile, holding period, and financial resilience.

Let’s Join Together to Bring Change to the World of Real Estate

Thinking about your next home?

relai scores every project on data, not paid placements, and it's free for buyers.