Hyderabad Real Estate: Navigating Market Saturation and Inventory Buildup

Hyderabad Real Estate: Navigating Market Saturation and Inventory Buildup

Over the past few years, Hyderabad’s real estate market has emerged as one of the most resilient in India — driven by IT expansion, infrastructure upgrades, and investor confidence. But even the strongest markets face moments of imbalance. Lately, the city has begun to show signs of saturation in certain premium and luxury segments, raising important questions about demand sustainability and pricing trends.

While overall housing demand remains steady, the rise in unsold inventory, especially in high-end zones, is quietly reshaping how developers, investors, and homebuyers are approaching Hyderabad’s property market.

1. Understanding the Current Market Phase

Hyderabad has enjoyed a long growth cycle — fuelled by stable governance, expanding employment opportunities, and improving connectivity through projects like the Outer Ring Road and Metro extensions. However, as developers rushed to meet growing demand, particularly in upscale areas like Financial District, Gachibowli, and Kokapet, the number of new luxury project launches began to outpace absorption rates.

Reports indicate that several premium properties now face higher holding times, with developers offering flexible payment plans or bundled amenities to attract serious buyers. In contrast, affordable and mid-income housing continues to sell consistently, driven largely by genuine end-users rather than speculative investors.

This imbalance marks the onset of a natural market correction phase — one that often follows a rapid period of expansion.

2. The Numbers Behind the Saturation

According to Knight Frank’s India Real Estate Report 2024, Hyderabad’s unsold housing inventory increased by nearly 15% year-on-year, primarily concentrated in high-ticket projects priced above ₹1.5 crore.

The city’s overall absorption rate remains healthy, but the luxury segment’s sales velocity has slowed, contributing to inventory buildup and marginal pricing pressure.

Meanwhile, rental demand and mid-segment sales remain robust, indicating that end-user confidence is intact. The market, therefore, isn’t witnessing a demand collapse — it’s experiencing a segmented slowdown.

This stage of moderation, though seemingly concerning, is actually essential for maintaining long-term market health. It helps cool overheated valuations and allows developers to reassess project feasibility before launching new inventory.

3. How Developers Are Responding

Developers are adapting quickly to shifting buyer behavior. Several leading builders in Hyderabad are now:

Rebalancing their portfolios by introducing smaller, right-sized apartments in high-demand areas.

Offering faster project completion timelines to avoid holding costs.

Increasing focus on sustainability and smart home features that appeal to modern buyers.

Reducing speculative launches in favor of customer-driven developments.

These adjustments signal a clear shift from volume-based growth to value-driven planning. The emphasis is now on creating demand-ready products instead of merely adding supply to the skyline.

This recalibration is particularly evident in micro-markets like Tellapur and Narsingi, where developers are actively adjusting pricing strategies and offering long-term maintenance plans to enhance buyer confidence.

4. The Buyer’s Perspective

For buyers, this market phase brings both opportunity and caution. On one hand, there’s more room for negotiation, with developers open to flexible pricing, add-ons, and better terms. On the other hand, the abundance of choices can lead to decision paralysis or hesitation if future pricing seems uncertain.

End-users — especially professionals working in the IT and BFSI sectors — continue to prefer completed or near-completion projects, prioritizing delivery certainty over speculative gains.

In contrast, investors have become more selective, focusing on rental yield potential rather than just appreciation prospects. Properties in areas with steady tenant demand — like Madhapur, Kondapur, and Manikonda — continue to perform well on yield stability, typically offering returns between 3–5% annually.

5. Implications for the Broader Market

Market saturation isn’t a crisis; it’s a correction signal that helps restore balance between supply and demand. The current trend in Hyderabad reflects the city’s maturity — moving from a purely growth-driven phase to a sustainable, demand-aligned phase.

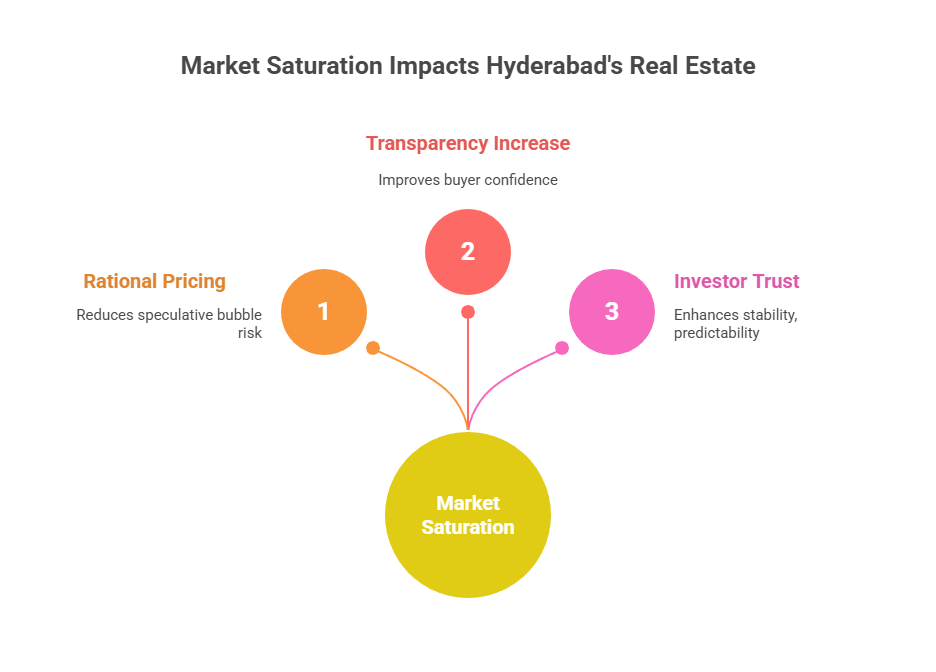

Some of the positive outcomes of this correction include:

More rational pricing, reducing the risk of speculative bubbles.

Higher project transparency, as RERA enforcement and digital platforms improve buyer confidence.

Improved long-term investor trust, since realistic pricing enhances stability and predictability.

Moreover, environmental regulations and responsible land use are becoming integral to development planning. The Telangana government’s active measures — such as clearing encroachments and improving stormwater infrastructure — are creating a cleaner, safer environment for future housing projects.

6. The Road Ahead for Hyderabad’s Real Estate

Looking ahead, the next growth cycle will likely be driven by data-backed planning, technology adoption, and sustainable design. Developers who align with these trends stand to benefit most as buyer preferences evolve.

Three key shifts will define this next phase:

Balanced Supply Pipelines: New launches will likely be moderated to match demand, avoiding speculative surges.

Tech-Integrated Transactions: Virtual tours, AI-based property recommendations, and online documentation are making real estate more transparent.

Sustainability as a Differentiator: Eco-friendly projects featuring solar energy, rainwater harvesting, and efficient design will dominate buyer preferences.

Hyderabad’s fundamentals remain strong — the city still boasts one of India’s most affordable price-to-income ratios among top metros and continues to attract both domestic and NRI buyers.

This temporary period of saturation isn’t a slowdown; it’s a pause for recalibration — ensuring the market grows on solid ground rather than speculative momentum.

FAQ Section

1. What is market saturation in real estate?

It occurs when the number of available properties exceeds current buyer demand, often leading to slower sales and stable or slightly corrected prices.

2. Why is Hyderabad facing inventory buildup?

A surge of luxury launches in high-demand zones like Kokapet and Gachibowli has led to an imbalance between supply and actual end-user absorption.

3. Is this situation bad for the market?

Not necessarily. It’s a natural part of market evolution that helps stabilize prices, improve quality, and promote sustainable development.

4. Which segments are still performing well?

Mid-segment and affordable housing continue to perform steadily, supported by working professionals and families seeking long-term ownership.

5. What should buyers focus on now?

Buyers should prioritize ready-to-move or near-completion projects in established locations with proven connectivity and rental potential.

Conclusion

Hyderabad’s real estate story is far from over — it’s simply entering a more mature chapter. Market saturation and inventory buildup, though challenging in the short term, are guiding the city toward a more transparent, efficient, and demand-aligned ecosystem.

Developers who adapt to these signals and focus on sustainable, right-priced projects will emerge stronger. Buyers, too, stand to benefit from this phase of rationalization, with more choices, clarity, and long-term value.

Relai – For right home.

Let’s join together to bring change to the world of real estate.

Thinking about your next home?

relai scores every project on data, not paid placements, and it's free for buyers.