Best Time to Buy a House: Market Timing vs Personal Readiness

One of the most common questions homebuyers ask is: “When is the best time to buy a house?” Market reports, price trends, and real estate news often encourage buyers to chase the “perfect timing.” But in reality, trying to time the market is rarely successful. For most buyers, the right time to buy is determined not by market cycles, but by personal readiness.

This article explores why market timing often fails, the financial signals that indicate you are ready to buy, and how to approach homeownership as a long-term decision rather than a short-term bet.

The Illusion of Perfect Market Timing

Many people believe that buying during a market dip guarantees savings. Similarly, some postpone purchases in fear of rising prices. While prices fluctuate, trying to predict the bottom or top of the market is extremely difficult.

Historical trends in Hyderabad show that property prices generally rise over the long term, with short-term volatility averaging 2–5% annually in residential segments. Even if you buy slightly “high” or “low,” your home appreciates over decades rather than months.

Relying on timing can lead to:

Indecision and missed opportunities

Buying too late or too early

Financial stress from last-minute leverage

Instead, personal financial stability should take priority over market speculation.

Why Timing the Market Often Fails

Market timing fails for several reasons:

1. Real estate moves slowly. Unlike stocks, property cannot be bought and sold in hours. Even during favorable market conditions, closing a deal can take months.

2. Prices are local, not national. Hyderabad has multiple micro-markets with differing price dynamics. A “downtrend” in one area may coincide with a “hot” market in another. Buyers focusing on general news often misinterpret local trends.

3. Emotional bias clouds judgment. Fear of missing out (FOMO) or waiting for a “correction” can result in delaying a purchase indefinitely.

4. Macro events are unpredictable. Policy changes, interest rate adjustments, and infrastructure announcements can shift market conditions rapidly, making timing even harder to predict.

Long-term value in property comes from location, layout, and ownership clarity, not short-term price swings.

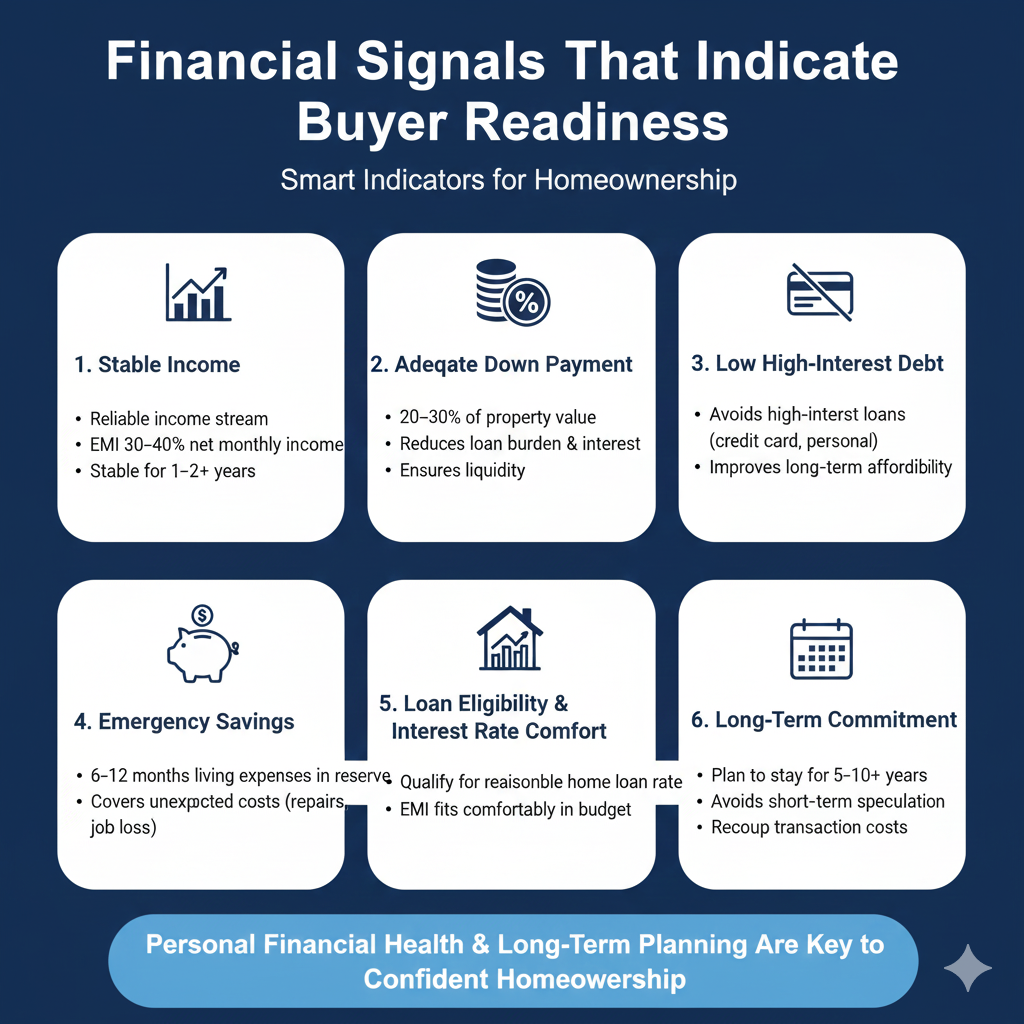

Financial Signals That Indicate Buyer Readiness

Instead of chasing market timing, buyers should evaluate personal financial readiness. Several indicators suggest that it is the right time to buy:

1. Stable Income

A reliable income stream ensures you can manage EMIs comfortably. Lenders typically recommend EMIs to be 30–40% of net monthly income. If your income is stable for at least 1–2 years, you are financially prepared.

2. Adequate Down Payment

Having 20–30% of the property value as a down payment reduces your loan burden and interest outgo. It also indicates that you have enough liquidity without depleting emergency funds.

3. Low High-Interest Debt

High-interest loans, such as credit card balances or personal loans, reduce your capacity to manage property-related expenses. Being debt-conscious improves long-term affordability.

4. Emergency Savings

Unexpected costs—maintenance, repairs, or temporary unemployment—can strain a homebuyer’s finances. Having 6–12 months of living expenses in reserve signals readiness.

5. Loan Eligibility and Interest Rate Comfort

Assess whether you qualify for a home loan at a reasonable interest rate. Even a slightly higher price is manageable if the EMI fits comfortably within your budget.

6. Long-Term Commitment

Buying a home makes sense only if you plan to stay for 5–10 years. Short-term speculation increases risk and reduces the likelihood of recouping transaction costs.

When Market Trends Can Be Considered

While personal readiness is paramount, market trends can still inform decisions:

Interest Rates: Lower rates reduce EMI burden, making certain periods financially favorable.

New Launches: Developers occasionally offer pre-launch or festive discounts, which may be worth considering if you are ready financially.

Infrastructure Announcements: Metro lines, flyovers, and IT park expansions can affect long-term appreciation.

However, these factors should enhance readiness, not replace it. They are secondary to personal financial stability.

Practical Steps to Prepare for Buying

Assess Your Budget: Include not just the purchase price but also registration, taxes, interior, and maintenance costs.

Check Your Credit Score: Higher scores improve loan eligibility and reduce interest rates.

Determine Loan Eligibility: Get a pre-approved loan to understand your financial bandwidth.

Prioritize Location and Type: Decide on city, micro-market, and apartment vs villa based on lifestyle and future plans.

Visit Multiple Properties: Evaluate layouts, amenities, and community management.

Consult Experts: Legal, financial, and real estate advisors help avoid mistakes that affect long-term returns.

Case in Point: Hyderabad 2025–2026

In Hyderabad, many first-time buyers waited for prices to drop in 2025, hoping for a “perfect entry.” Meanwhile, ready-to-move apartments and pre-launch projects saw stable demand due to financial readiness among buyers who acted without delay. These buyers benefited from better property selection and smoother handovers, rather than relying on market timing.

This example shows that personal readiness outweighs market speculation, even in volatile conditions.

FAQ

Q1: Is there a perfect time to buy a house in Hyderabad?

A1: No. Long-term value depends more on personal financial readiness than short-term market fluctuations.

Q2: What financial signals indicate readiness to buy?

A2: Stable income, sufficient down payment, low high-interest debt, emergency savings, loan eligibility, and long-term commitment.

Q3: Can market trends influence buying decisions?

A3: Interest rates, developer offers, and infrastructure announcements can enhance decisions but should not replace personal readiness.

Q4: Why does trying to time the market often fail?

A4: Real estate moves slowly, prices vary locally, and macro events are unpredictable, making market timing unreliable.

Q5: How should buyers approach property selection?

A5: Focus on location, micro-market trends, home layout, and long-term livability rather than short-term price swings.

Conclusion

The “best time” to buy a house is not when headlines suggest or when prices dip temporarily. It is when your finances, lifestyle, and long-term plans align. Timing the market is unpredictable and rarely yields the benefits buyers hope for.

Key signals of readiness include stable income, sufficient down payment, low high-interest debt, emergency savings, loan eligibility, and long-term commitment. Secondary considerations, like interest rates or developer offers, should enhance your decision rather than dictate it.

At Relai – For right home, we focus on helping buyers identify true readiness, evaluate options across Hyderabad, and make confident decisions that balance lifestyle, investment, and financial prudence.

Let’s Join Together to Bring Change to the World of Real Estate.

Thinking about your next home?

relai scores every project on data, not paid placements, and it's free for buyers.