India’s Housing Affordability Crisis and the New Age of First-Time Buyers

India’s Housing Affordability Crisis and the New Age of First-Time Buyers

India’s housing market is going through a major shift. Prices are rising faster than incomes, loan rates remain elevated, and urban land shortages are pushing families into the suburbs. At the same time, people are starting their homebuying journey later than ever before. This trend mirrors global patterns, where affordability pressures have delayed first-time ownership across major economies.

In India’s big cities—Hyderabad, Mumbai, Bengaluru, Pune, and Chennai—the gap between household income and home prices is at its widest point in two decades. For many families, the dream of buying a home is taking longer to achieve.

This blog breaks down what is driving this shift, how it compares to global trends, and what this means for future buyers.

Why First-Time Buyers Are Getting Older in India

India hasn’t reached the extreme levels seen in countries like the US—where the median buyer age has surged to 59 and first-time buyers now average around 40—but the direction is similar. In Indian metros, the typical first-time homeowner is now in their early-to-mid 30s, compared to the mid-20s just a decade ago.

Three forces explain this shift:

1. Prices Are Rising Faster Than Incomes

According to the Knight Frank Affordability Index (Knight Frank Housing Affordability Report), affordability in cities like Mumbai, Hyderabad, and Bengaluru has weakened due to:

20–40% price appreciation post-2021

higher construction costs

premium land values within city limits

Even with stable job growth, salaries have not kept pace with property values.

2. Loan Rates Remain Higher Than Pre-Pandemic Levels

While rates may ease gradually in 2025, current levels still reduce purchasing power.

For every 1% rise in rates, a buyer loses 7–8% affordability, pushing younger families into postponement.

3. Lifestyle Delays Are Shifting Homebuying Timelines

People today are:

marrying later

changing jobs more often

prioritizing renting near work rather than buying far away

waiting for income stability before committing to a loan

These choices naturally delay the first home purchase.

The Inventory Paradox: More Listings, But Still Not Enough

Globally, several markets report rising inventory and falling demand. Threads on X highlight metrics such as:

20 straight months of rising listings

nearly 500,000 more homes for sale than buyers

homes sitting unsold for 60+ days

average discounts of $25,000

India isn’t experiencing the same oversupply.

Instead, India faces a different paradox:

India has more inventory than last year, but still has a structural shortage.

According to JLL and ANAROCK reports (ANAROCK Housing Market Report), India has a shortfall of around 30 million housing units, concentrated mainly in:

affordable housing

rental housing

migrant worker accommodation

urban-core demand pockets

So even as some developers release new supply, the demand backlog stays large.

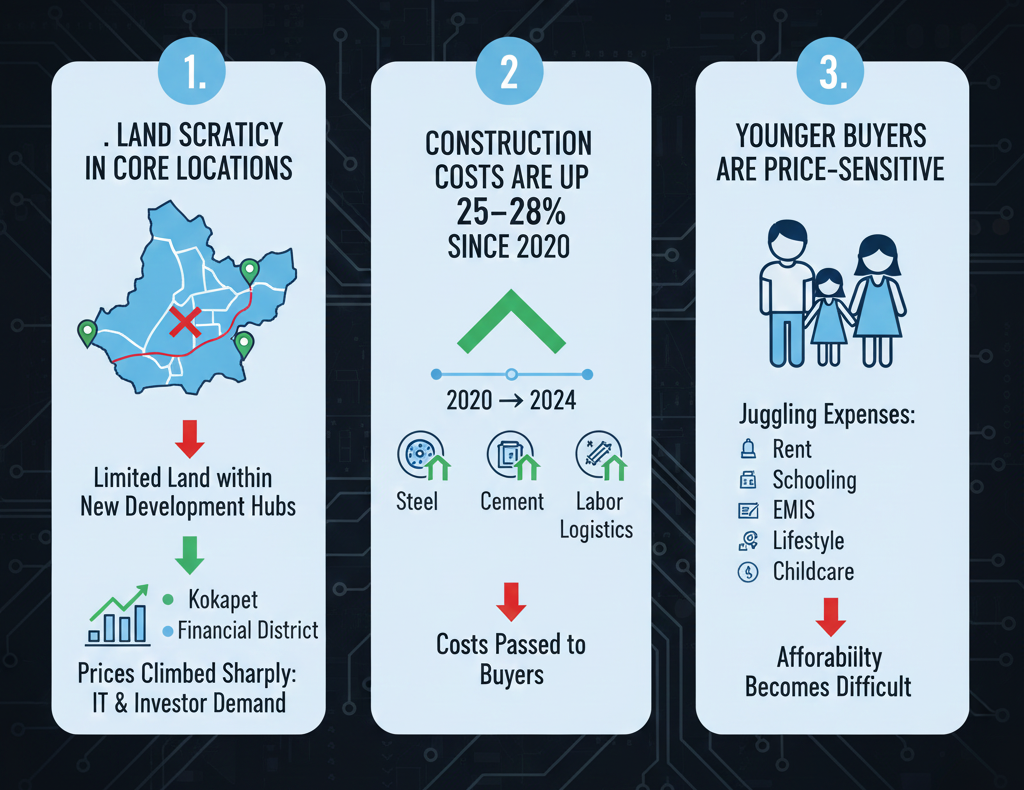

Why Affordability Is Under Pressure in Indian Metros

1. Land Scarcity in Core Locations

In cities like Hyderabad, the areas within the Outer Ring Road (ORR) have limited land available.

This pushes development into:

Kokapet

Financial District

Narsingi

Kondapur

Bachupally

While new supply is strong, prices have climbed sharply due to IT expansion and investor demand.

2. Construction Costs Are Up 25–28% Since 2020

Steel, cement, labour, and logistics have all become costlier. Developers pass a portion of these costs to buyers.

3. Younger Buyers Are Price-Sensitive

With many Indians in the 25–35 age group juggling:

rent

EMIs for schooling

lifestyle expenses

childcare costs

affordability becomes more difficult.

How the Age Shift Impacts Families

When homebuying moves from the late 20s to early 30s — or even mid-30s — the effects touch multiple parts of life:

1. Delayed Family Planning

People want stable housing before starting or expanding their families.

Rising prices push these decisions further.

2. Shorter Loan Tenure

A home bought at 35 gives fewer working years to repay.

This raises EMI pressure unless the buyer makes a higher down payment.

3. Higher Lifetime Housing Costs

Delaying purchase often means buying at higher prices later.

4. Increased Reliance on Parental Support

More Indian buyers today use:

joint loans

parental co-applicant backing

family-assisted down payments

This was less common 15–20 years ago.

Will Affordability Improve Soon?

Global analysts predict mortgage rates may ease to around 5.5% by mid-2025.

In India, any rate reduction will help buyers, but it won’t fully solve affordability because:

demand in key metros remains strong

jobs continue to centralize around high-value districts

urban land remains limited

construction costs are unlikely to fall

Experts at Colliers and JLL note that India’s housing demand is structurally stable, driven by:

IT sector growth

rising incomes

nuclear family preferences

suburban expansion

post-pandemic preference for owned homes

This means demand will hold even if affordability stays stretched.

X (Twitter) Buzz: The Push for Policy Fixes

Trending conversations on X link the affordability crisis to larger economic themes.

People argue that India must:

boost new-home construction in affordable and mid-income segments

improve clarity on land titles

accelerate infrastructure to open up new micro-markets

push faster approvals via online systems

incentivize rental housing

reduce acquisition delays for large townships

The belief is simple:

More supply + faster delivery = better affordability.

FAQ Section

1. Why are first-time buyers getting older in India?

Rising prices, higher EMIs, delayed marriages, and preference for renting near workplaces have shifted homebuying from mid-20s to early or mid-30s.

2. Is India facing a housing shortage or oversupply?

India faces a structural shortage, especially in affordable and mid-income categories, even though some premium projects show temporary oversupply.

3. Will affordability improve in 2025?

If interest rates soften, affordability may improve marginally. But construction costs and demand levels keep prices elevated.

4. Why are millennials and Gen Z delaying home purchase?

Unstable job locations, lifestyle priorities, high rents near workplaces, and difficulty saving for down payments are key reasons.

5. What can improve affordability in India?

More supply, quicker approvals, expanded suburban infrastructure, better rental ecosystems, and targeted incentives for first-time buyers.

Conclusion

India’s housing affordability challenge is reshaping the age and profile of first-time homebuyers. Rising prices, elevated loan rates, and limited central-city supply have pushed many buyers to delay their first purchase. While global markets show signs of cooling, India’s demand remains structurally strong due to urbanization, income growth, and demographic pressures.

As India moves toward a more urban future, solving affordability will require coordinated action—stronger planning, faster supply creation, and better financing pathways. The goal is simple: ensure families can buy homes earlier, without compromising long-term financial stability or life decisions.

Thinking about your next home?

relai scores every project on data, not paid placements, and it's free for buyers.